Mortgage Loan Originator

Matthew Brown

NMLS 957820

matthewbrown@mutualmortgage.com Cell: (443) 624-2556 Office: (410) 226-8972x818972 Apply NowMatthew Brown believes in the value of home ownership and understands the importance of finding the right loan to achieve your goals. With a deep understanding of the many loan programs Mutual of Omaha Mortgage offers, Matthew works closely to understand each client’s needs, and find mortgage solutions to best fit their financial goals.

Throughout the borrowing process you can count on Matthew to be a trusted guide through the loan process and ensure that your loan is completed thoroughly, accurately, and on time. Matthew Brown is backed by a dedicated team of operational experts and state-of-the-art technology designed to make the loan process easy and efficient.

Whether you’re looking to purchase, refinance, or take out a home equity loan, Matthew Brown will be happy to talk with you about your current needs, and your long-range goals in order to find a financing program that works best for you. Contact Matthew today to get started.

See What Our Customers Have to Say

132 Reviews

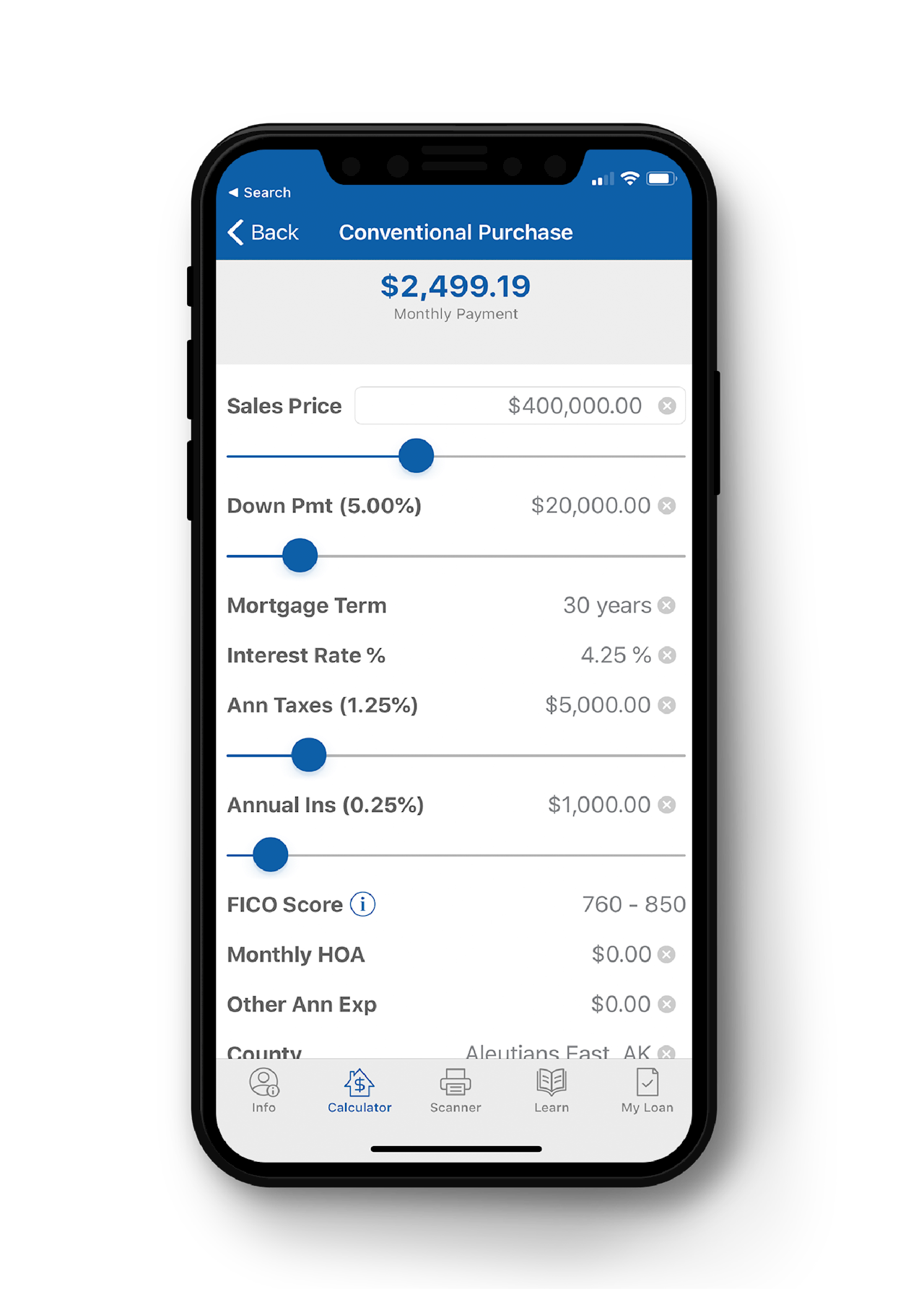

Mortgage Tools at Your Fingertips

Enjoy having all your mortgage tools in one place and move the process forward with a click.

![]() Simply tap to apply from anywhere

Simply tap to apply from anywhere

![]() Click to calculate the estimated cost of your mortgage payments

Click to calculate the estimated cost of your mortgage payments

![]() Scan and send loan documents with ease and security

Scan and send loan documents with ease and security

![]() Check your loan status and take the mystery out of the process

Check your loan status and take the mystery out of the process

![]() Direct access to your loan officer

Direct access to your loan officer

Mortgage solutions to fit your needs

Why choose Mutual of Omaha Mortgage for your home loans?

Working with a brand you know and an advisor you trust

Personalized service through the loan process from an experienced mortgage expert

Manage the entire loan process from anywhere with our easy-to-use mobile app

Mortgage Calculators