Mortgage Loan Originator

Ken Miller

NMLS 110090

kmiller@mutualmortgage.com Cell: (410) 952-4122 Office: (410) 952-4122 Apply NowI have more than 20 years of mortgage origination experience and am so excited to be part of the Mutual of Omaha Mortgage team. We offer a great selection of loan products. My philosophy is focused on personalized service and providing a smooth loan process for all parties. Creating Raving Fans is what it’s all about.

I take extreme pride in the fact that realtors prefer me as their mortgage partner because of my high level of knowledge and the quality of service I provide to each client. From start to finish, I will be attentive and detailed in addressing your unique mortgage needs. I am committed to you and will return each call, text and email promptly during the loan process. I believe in taking customer service to a whole new level and will attend your closing, to provide that extra peace of mind. My goal is to turn each client, buyer and realtor into a Raving Fan.

Whether refinancing an existing mortgage, buying a first home, or purchasing a vacation or investment property, I will work with a steady level of enthusiasm, honesty, and professionalism. Call me today to explore your mortgage needs.

See What Our Customers Have to Say

3 Reviews

Mortgage Tools at Your Fingertips

Enjoy having all your mortgage tools in one place and move the process forward with a click.

![]() Simply tap to apply from anywhere

Simply tap to apply from anywhere

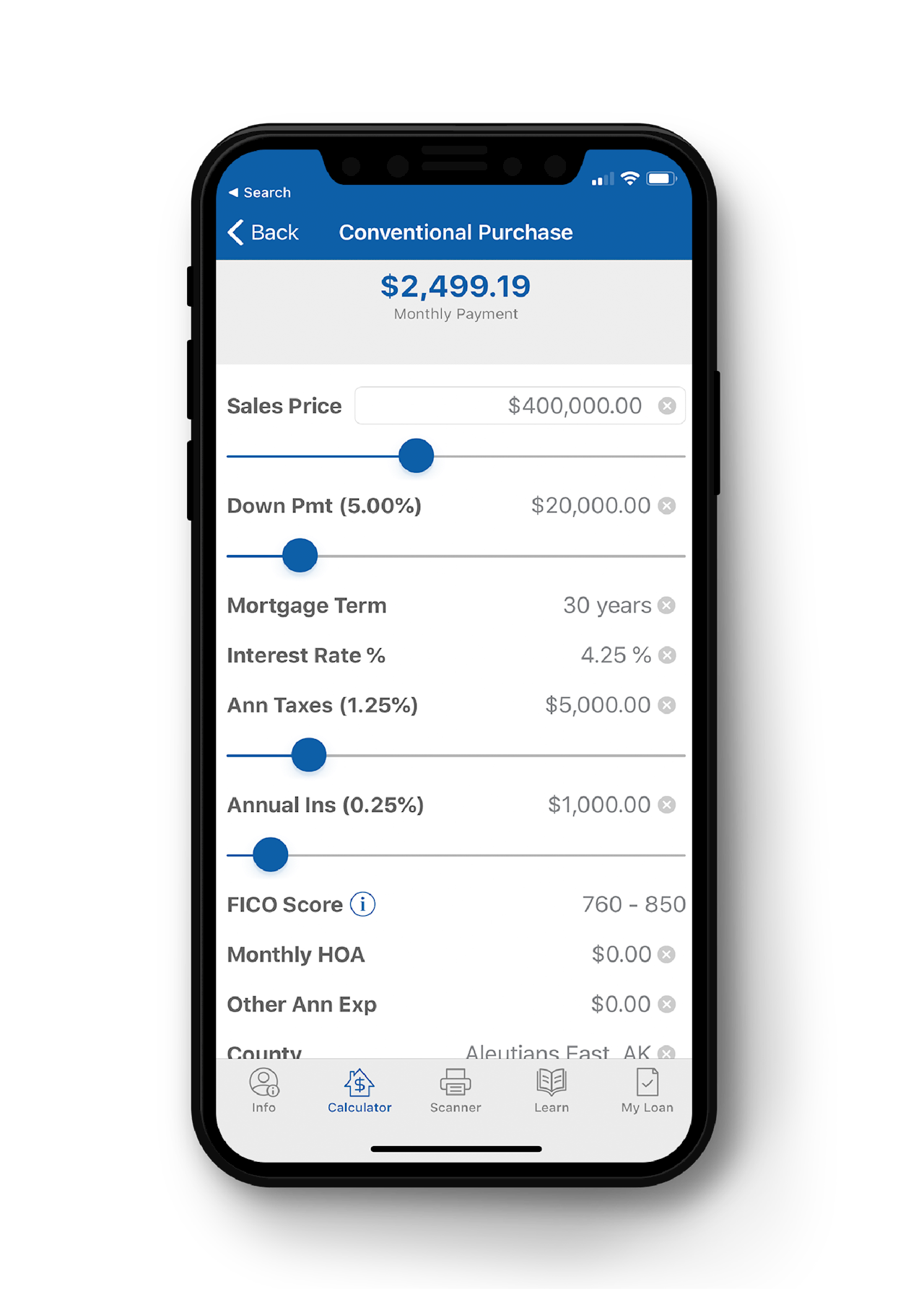

![]() Click to calculate the estimated cost of your mortgage payments

Click to calculate the estimated cost of your mortgage payments

![]() Scan and send loan documents with ease and security

Scan and send loan documents with ease and security

![]() Check your loan status and take the mystery out of the process

Check your loan status and take the mystery out of the process

![]() Direct access to your loan officer

Direct access to your loan officer

Mortgage solutions to fit your needs

Why choose Mutual of Omaha Mortgage for your home loans?

Working with a brand you know and an advisor you trust

Personalized service through the loan process from an experienced mortgage expert

Manage the entire loan process from anywhere with our easy-to-use mobile app

Mortgage Calculators