VP of Mortgage Lending & Corporate Outreach

Nick Zbair

NMLS 441826

nzbair@mutualmortgage.com Cell: (248) 240-0167 Office: (888) 524-3452 Apply NowNick Zbair has been in the mortgage industry for over 12-years, originating residential mortgage loans in all 50 states. During that period of time, he has helped more than 2,000 people refinance and purchase new homes. He prides himself on 24-hour client service, having his client’s best interests at hand and making sure that all of his clients are always in the best loan programs.

Nick believes in having a great attitude at all times and putting in 100% into everything he does to accomplish his goals. While most today call Nick a Master of his field, he makes it a point to continue learning and making himself better in every way.

Some of Nick’s hobbies include exercising, painting, reading and writing. He’s a fan of all movie genres from comedies to dramas and loves a great story.

See What Our Customers Have to Say

251 Reviews

Mortgage Tools at Your Fingertips

Enjoy having all your mortgage tools in one place and move the process forward with a click.

![]() Simply tap to apply from anywhere

Simply tap to apply from anywhere

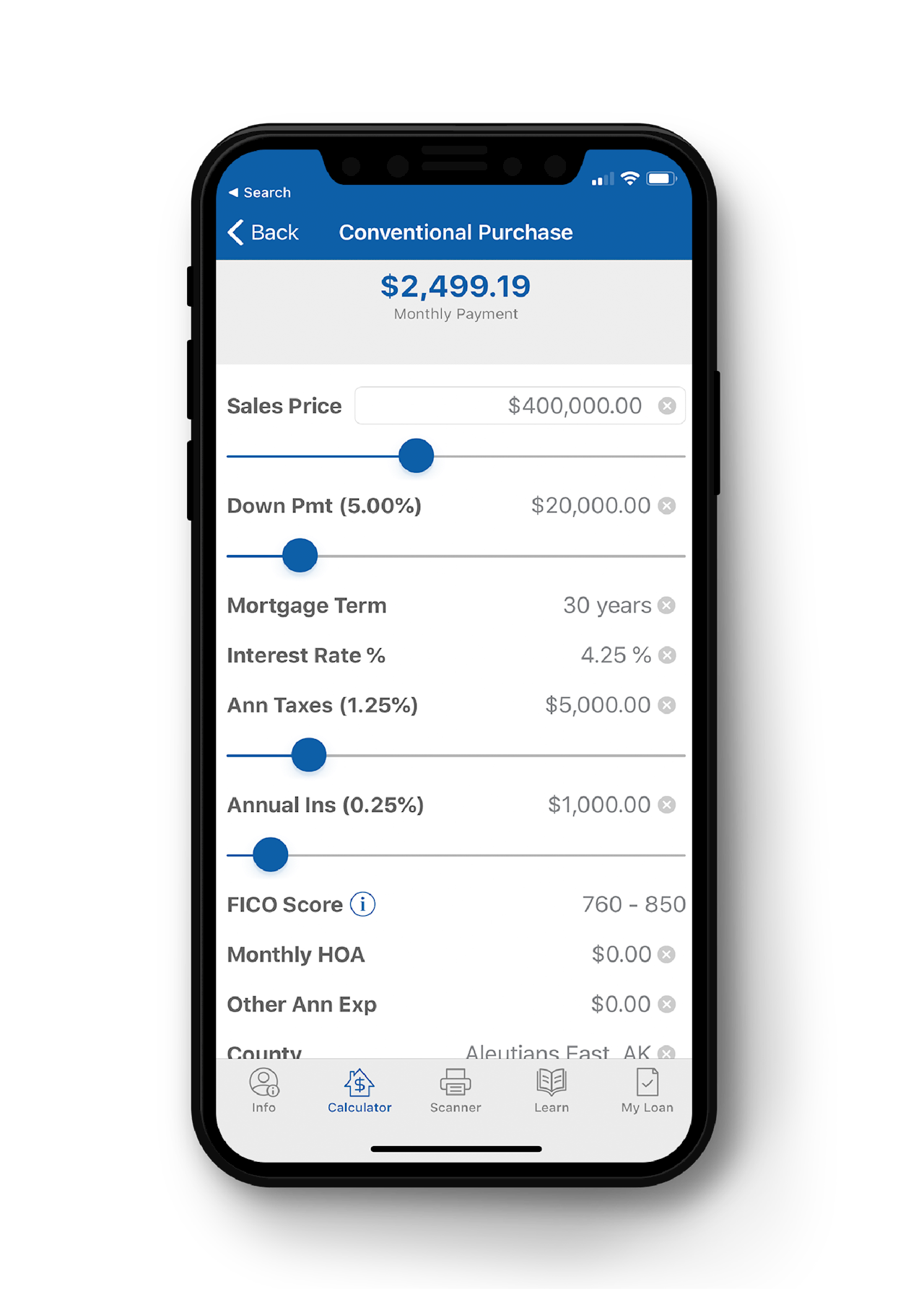

![]() Click to calculate the estimated cost of your mortgage payments

Click to calculate the estimated cost of your mortgage payments

![]() Scan and send loan documents with ease and security

Scan and send loan documents with ease and security

![]() Check your loan status and take the mystery out of the process

Check your loan status and take the mystery out of the process

![]() Direct access to your loan officer

Direct access to your loan officer

Mortgage solutions to fit your needs

Why choose Mutual of Omaha Mortgage for your home loans?

Working with a brand you know and an advisor you trust

Personalized service through the loan process from an experienced mortgage expert

Manage the entire loan process from anywhere with our easy-to-use mobile app

Mortgage Calculators